Conversion Cost

Conversion cost is the forgone economic resources to ensure that raw materials are transformed in to finished inventory or goods. As the name suggests, the term conversion means change, alteration, or translation of an item or raw material to a finished good.

This type of cost element is based on under the critical decision management has to make. It is at appoint when the management is at the cross-road and the decision made will result to key turn of events. Under this criterion we have;

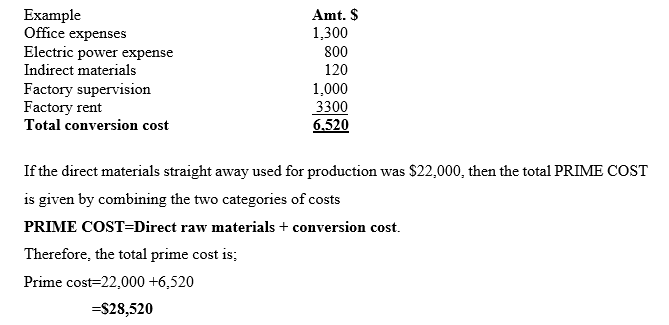

Cost elements in this classification is associated with the resources that were directly used to add form utility to the raw materials. Such resources aid in transforming the row form of raw materials to useful form of a product. Hence these resources forgone are referred to as conversion cost. They comprise direct labor wages, and manufacturing overhead. In other words, conversion cost is the prime cost less direct raw material cost for we should not forget that it is the raw materials which are being converted by the other direct inputs during production. You should also note that other conversion costs will include any normal wastages and gains during the conversion process such as gains and losses in weight or volume of direct material arising due to formation process.

FORMULA

Conversion Cost = Direct Labour + Indirect Labour+ Production Overheads

Therefore, any costs incurred or paid in ensuring that final output is accomplished, is termed as conversion cost as indicated below.

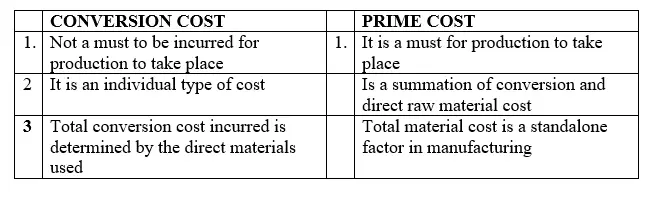

Differences Between Conversion Cost And Prime Cost

Advantages Of Conversion Cost

- It is a tool for monitoring the efficiency level of inputs added on the raw materials.

- Help in pricing of the final product

- Help in optimal allocation of the economic resources

- Elimination of wastage of raw material for from past experience of the conversion cost consumed, it is possible to know the amount of raw materials to purchase or extract.

- Managers and business owners sometimes use conversion costs to determine if any waste can be eliminated

Disadvantages Of Conversion Cost

- Not applicable where the production does not require any kind of conversion process

- Not commonly used by the small manufacturers. It is always ignored because it is difficulty to compute.

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.