Differential Cost

Definition

Differential cost is the change in cost due to change in a cost driver. The change may either be an incremental or a declining one and it is that change in cost which determine the kind of decision to be made by the decision maker. This cost element under this criterion is pegged on the critical decision the management has to make. It is at appoint when the management is at the cross-road and the decision made will result to key turn of events. Under this criterion we have various cost drivers such as;

- Level of production/output

- Time duration

- Change in fixed cost

- Change in variable cost

- Adoption of alternative course of action

For each cost driver case 1-4 above an illustration has been used to show the scenario of each outcome. But all the results gotten represent differential cost

1.1 Illustration 1

1.1.1 Change in level of production;

- Suppose the cost of producing 1000 units of banana chips is $500 and the cost of producing 1200 is $560. Then the differential cost (i.e., an increase) to be paid to produce more or extra 200 units is $60 (560-500).

- Suppose the cost of manufacturing ten (10) cartons of biscuits is $123 and the cost of producing eight (8) cartons is $89. Then the differential cost is $34 ((i.e., a decrease).

1.2 Illustration 2

1.2.1 Case of change in time

- The cost of doing extra tuition to the candidate class for one week is $100 and the cost for two weeks turn out to be $500. Therefore, the differential cost of doing tuition for an extra one week is $400.

1.3 Illustration 3

1.3.1 Case of change in fixed cost

If the fixed cost for producing one motor bike has changed from $130 to $330 for producing extra 5 motor bikes. Then the differential cost for manufacturing extra 5 bikes is $200(i.e., 330-130)

1.4 Illustration 4

1.4.1 Case of Change in variable cost

Due to Russian-Ukraine war, the cost of fueling a car of 1800 cc to cover 30 kilometers to school changed from $122 to $165 to cover a distance of 45 kilometers. The differential cost is $43 (i.e., 165-122) to cover extra 15 kilometers (45-30).

1.5 Illustration 5

1.5.1 Case of Adopting of alternative course of action

Pablo road constructors has been using Double XX plant machinery to prepare 1000 kilometers of road at a cost of $250. A new plant machinery known as Double TT which is using new technology is now in use to do the same 1000 kilometers at $215. The differential cost is $35 less than the initial case. Hence a saving.

1.6 Marginal cost

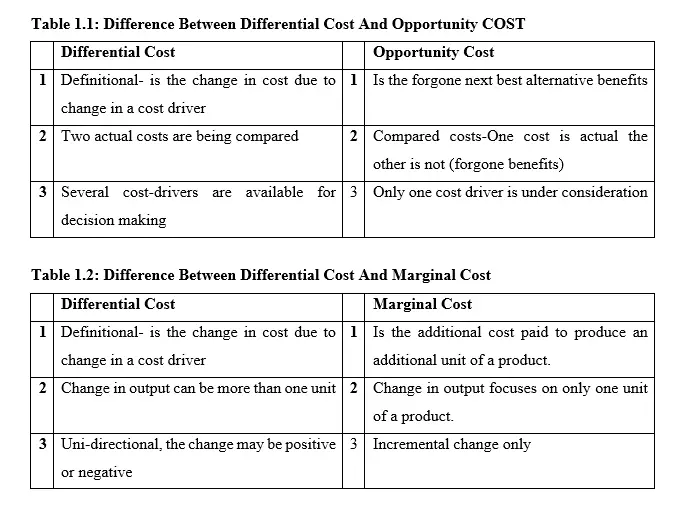

It should be noted that if one need to consider the total cost of production of product X in this week and that of the following week and establish the difference between the two values. This term in other words is what Economists refer to marginal cost. For your information, in Economics, for a profit maximizing firm an organization should produce efficiently and effectively at a point where differential cost is equal to differential revenue. In other words where marginal cost is equal to marginal revenue (MC=MR).

Characteristics Of Differential Cost

- Differential cost is as a result of critical decision to be made by the management

- Differential cost is Uni-directional. In other words, it does not mean the change is positive or negative. It takes whichever direction.

- It is common in future time horizon

Advantages Of Differential Cost

- Decision making

Differential cost is a tool for decision making generally especially where there is strategic focusing for the whole organization.

- Resource allocations

This tool is good in guiding the management on how the scarce resources can be optimally assigned on tasks of the business to get better results.

- Capital project selection

Differential cost is a tool for ranking the capital project on the basis of the cost incurred or paid.

- Tapping of investment opportunities

Differential cost guides the management on the extra required cost needed to tap a wind fall of a project or to know the cost saving a firm can build in two different circumstances.

Disadvantages Of Differential Cost

- Confusing with other similar concepts

Differential cost is also synonymously referred by some users as marginal cost while others call it opportunity cost. All these assumptions are not correct and hence no way two firms or more can compare performance.

- Complex in computation

It is not easy to computer the correct value of differential cost for the requirements are diverse based on the user interpretations they make. Such that at the end of the day they have different opinions.

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.