Material Cost: Introduction; Objectives; Definition; Raw Material Inventory Management.

1.1 Introduction

This article focuses on the thematic issue of material cost. Material cost is one of the mainstream cost elements that compose a final product produced by the firm. In this article, there are objectives to be attained by the learner.

1.1.1 Objectives

The main objective of this cost accounting topic on material cost is to comprehend the scope and nature of this concept. The specific objectives are that the learner will be able to;

i). Distinguish between material cost and other costs that entail production of a product.

ii) Describe the steps of managing material inventory in a business set up.

Definition; Material cost is the monetary value of consumed raw materials in production process. The cost incurred may be through purchase of the raw materials or cost of extracting the raw materials from their natural state. The rate of cost per unit of raw materials used depend on the nature of the materials used in production.

For a cost accountant to determine or compute the material cost used in production of a particular product, many logistics will have to be put in place. Therefore, establishment of the total material cost cuts across many activities that have been discussed in this article. These logistics have been discussed under inventory management system which include and not limited to;

Planning, organizing, coordinating, staffing and controlling of material inventory activities of an organization. This discussion is pegged on the value chain management approach where by the learner/entrepreneur will comprehend of the activities translating to material cost through learning the entire supply chain, from purchasing to production to end sales. This is because the aim of incurring or paying for material cost is to convert them in to work in progress or finished goods for selling purposes. The main focus in this study is the management related activities of raw material inventory for manufacturing or production purposes.

Since the focus of determination of material cost trickles down to inventory, the specific objectives of inventory management that the learner will achieve is to;

- Describe the 9 stages followed in purchasing of inventory.

- Describe the 4 stages followed in issuance of inventory.

- Explain the concept of inventory storage and types of stores.

- Explain the uses or functions of recordkeeping documents used in inventory management.

- Explain the concept of inventory control and the different inventory levels.

- Compute Economic Order Quantity and interpretate the model.

- Relate the mathematical and graphical EOQ model.

- Define or and explain the EOQ related terms useful in computation of EOQ model

- Explain the advantages and disadvantages of EOQ model.

Raw Material Inventory Management

Inventory management of raw materials is under the purchasing department especially in big organizations. The department is headed by the purchasing manager who is responsible of obtaining all acquisitions be it raw materials, consumable stores, spare parts of machinery and even purchases for reselling purposes. The purchasing manager does the planning on how to ensure that the requisitions are received in time and in the right quantities and qualities. He/she also organizes for proper handling of those purchases and how they will be utilized in the future to optimize output. The manager also undertakes the control function of ensuring that the actual activities related to inventory such as purchasing, inventory quality and quantity is compared with the expected levels or standards so as to deal with variances whether favorable or adverse.

Control function is very important because any adverse variance such as purchase of excess raw materials may result to wastage especially for perishable goods or may result to additional expenses such as storage or holding costs. This may make the inventory more costly. Similarly, purchase of less inventory may imply losses such as failure to meet orders of the customers which may result to sales losses. Further, purchase of inferior raw materials may imply that quality of the final product may be low hence lose customer loyalty. This will lead to reduced sales hence translate to reduced profitability of the firm. Therefore, control function is key for it is a protector guard to the firm. So, the purchasing department need to lay down purchasing polies that can enable the firm to achieve the following specific objectives, namely;

- Purchase of inventory cheaply without compromising the quality thereof.

- Timely purchases to avoid shortages of raw materials which may lead to less supply in the market.

- To purchase the right quantities.

- To ensure that the firm’s products are in the market limelight to avoid loss of market share.

- The next step as a learner/entrepreneur is to understand what is inventory management and the procedures thereof.

2.1 Inventory Managerial Procedures

Inventory management entails all the functions of planning, organizing, coordinating and controlling of inventory related activities so as to achieve the objectives of reducing inventory management costs and on the other hand maximize organization’s sales turnover by efficiently and effectively meeting customer demand. Therefore, inventory management system is composed of various procedures and processes which work in harmony to achieve the set inventory management goals. One of the main goals of the business is to determine the material cost per unit of the product it has produced.

Determination Of Material Cost Per Unit

All the endeavors we have done to evaluate raw material inventory is with a purpose. The aim was to determine a definite way of establishing the actual cost of raw materials used in production of a complete unit of a product. But the big question is, what is Material Cost? This term was defined in the initial stage of introducing this concept. Just to remind you again, let us have a recap of this definition.

Definition: Material cost is the monetary value of consumed raw materials in production process. The cost incurred may be through purchase of the raw materials or cost of extracting the raw materials from their natural state. The rate of cost per unit of raw materials used depend on the nature of the materials used in production. To determine the cost of raw materials used, the right Key Measurement Indicator need to be used.

Now, establishment of the cost of raw materials used in producing or manufacturing a unit of a complete product, may be simple or complex based on the information provided by the business. Determination of the cost of raw materials per unit in an organization is the goal to be achieved at the end of all the activities that surrounding raw materials such as purchase and valuation of inventory. Most of the times, if the raw materials were fully used up to produce completed units of a product, its okay. This can be simple to determine the cost per unit. However, there are three main scenarios which govern on the procedure to follow to determine the material cost per unit.

- Where no opening and closing inventory of raw materials.

- Where there is opening and closing inventory of raw materials.

- Where there is opening and closing inventory of Work in Progress (WIP).

Scenario “a”: Where there is no opening and closing inventory of raw materials.

Where there is no opening or closing inventory of raw materials, determination of raw material cost per unit is simple.

Example one

Product: Banana chips; produced in terms of 50g packets;

Requirements: 50g of banana pieces @ $1.5 per gram, material cost turns out to be $1.5 to produce a 50g packet of banana chips.

Example two

Product: Shirt; produced in terms of one unit of shirt;

Requirements: 11/2 meters @ $2.0/meter, material cost turns out to be $3.0 to make one shirt

Conclusion; You can see different material unit measure is used for different products. This means that the entrepreneur/student needs to identify the best measurement indicator so as to avoid wrong estimations of cost thereof and also, determination of material cost per unit is very simple.

Scenario “b”: Where there is opening and closing inventory for raw materials

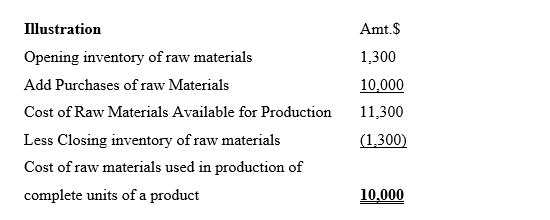

In this case, the procedure is a little bit complicated although not much if you as a student or entrepreneur are careful about the logic behind the approach. To determine the material cost per unit, you need to appreciate that the cost incurred to purchase raw materials may not all reflect in the final product for sometimes there may be some unused raw materials at the end of the financial period. Such unused raw materials at the end of the period are referred to as closing inventory of raw materials. And the same materials turn out to be the opening inventory of raw materials in the proceeding period. This is where the seven methods of raw material inventory valuation apply. The following procedure is used and mark you it is similar to the one used in financial accounting when determining the cost of sales.

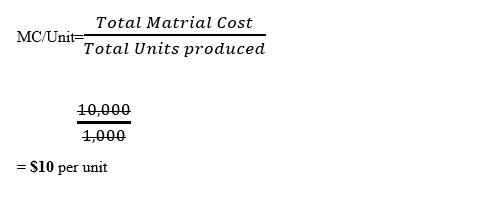

Let us assume that the total complete units produced were 1000. Then the material cost per unit would be;

Scenario “c”: Where there is opening and closing inventory of Work in Progress (WIP)

Work in Progress raw materials is partially processed raw materials where by the raw materials are less than 100% used up in production of final product.