Material Inventory Valuation Procedure-Base Stock Valuation Method

Specific Objective; Definition; Base Stock Valuation Method; Example

Specific Objectives

This article is guided by the following 2 specific objectives. The learner/user of this article will be able to;

- Define the term base stock valuation method

- Compute inventory monetary value using base stock valuation method.

Base Stock Valuation Method

Definition

Base stock valuation method entails identification of a certain level of inventory which is assumed to retain the original cost of purchase even if there are dynamics of price changes. So, this methodology of inventory valuation assumes that this set aside inventory level is retained and the organization should not allow demand to push for sale or usage of that that inventory. Actually, that level of inventory is taken like the safety stock that we all know. Then the next key point as pertains base stock, is that as far as which inventory to be dispatched first, the FIFO method is relied upon.

Example

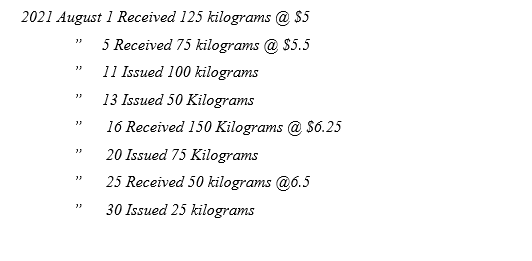

Polite Notice (PN) company ltd provided you with the following inventory details for the month of August 2021

Required

Using the above information, determine the monetary value of closing inventory at the end of August under Base Stock valuation method.

Solution

Explanation of inventory Issuance of Base Stock above

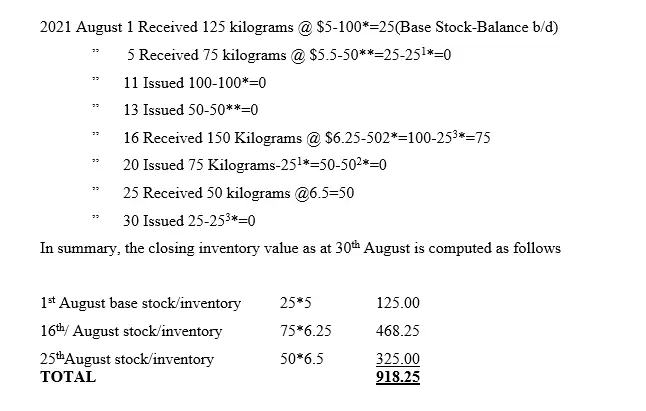

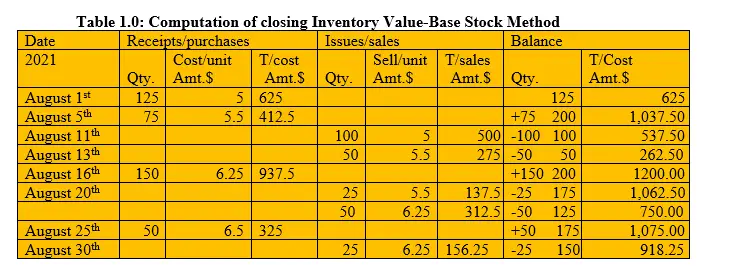

Note: That, total units of inventory before issuance began was 200 units made up of 1stAugust 125 units plus 5th August 75 units. Then…

11th August the first 100 units of inventory was issued and was from 125 batch of units of inventory received on 1st August. Since this is base stock method, the 25 units of inventory was retained as the base stock/inventory.

Let us now deal with the rest of the inventories knowing that there is already 25 used as base inventory:

On 13th August, next issuance of 50 units of inventory was made and was from the inventory batch of 75 units received on 5th August. The 5th August batch had a balance of 25 units. On 16th August, the organization received additional 150 units of inventory. So, the total units of inventory were 25+150=175. On 20th August, another issuance of 75 units of inventory was made. 25 units were picked from the 5th August batch which had a balance of 25 units. This batch therefore got exhausted. The 50 units to be issued was from the 16th August batch where by the balance left was 100 units. Then another additional inventory was received on 25th August of 50 units translating to a total of 150 units of inventory. Then the last issuance was 25 units of inventory and it was picked from the 16th August 150 batch of units which is currently having a balance of 100 units. So, after issuance it is now 75 units remaining.

Note that the superscripts (i.e., *, ** ,1*, 2* and 3*) used below will guide you on which inventory batch each issuance was picked from. This inventory analysis is a computational proof of monetary value of closing inventory as at 30th/08/2021.