Material Inventory Valuation Procedure-Last In First Out (Lifo) Inventory Valuation Method

Specific objective; definition; lifo method of inventory valuation; example

Specific Objectives

This article is guided by the following 2 specific objectives. The learner/user of this article will be able to;

- Define the term LIFO inventory valuation method

- Compute inventory monetary value using LIFO method

Last In First Out (Lifo)Inventory Valuation Method-Lifo

Definition

LIFO method is an inventory valuation approach which considers valuation of closing inventory at the end of the financial period with the assumption that the inventory elements which are forming the closing inventory are from the earlier purchased goods. As the name suggests, the method assumes that recent raw materials received in the business or factory are the first ones to be consumed in manufacturing or production. Therefore, by the time stock taking activity is being undertaken, the materials available are the ones which were received in past period (i.e., the oldest).

Example

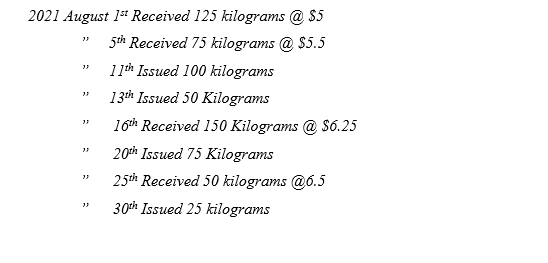

Polite Notice (PN) company ltd provided you with the following inventory details for the month of August 2021

Required

Using the above information, determine the monetary value of closing inventory at the end of August under LIFO method.

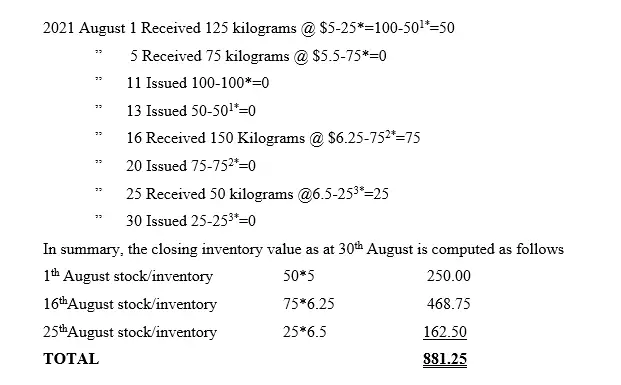

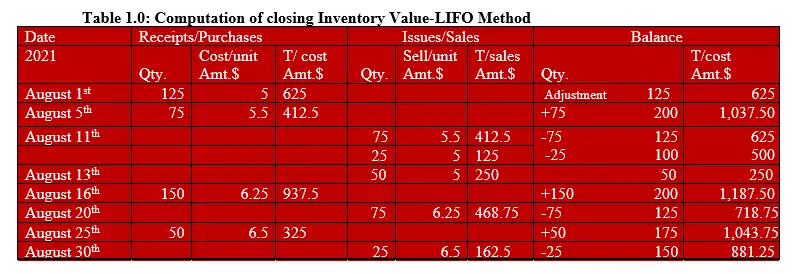

Solution

Explanation of Inventory Issuance for LIFO Method above

Note: That, total units of inventory before issuance began was 200 units made up of 1stAugust 125 units plus 5th August 75 units. Then…

11th August the first 100 units of inventory was issued and was from the 5th August 75 batch of units of inventory received. The balance was picked from the 1stAugust inventory. The second issuance was of 50 units and was picked from the 1stAugust inventory which had an existing balance of 100 units. An additional inventory was received on 16thAugust of 150 units of inventory. The third issuance was made of 75 units and were picked from the recently received inventory of 16thAugust. This resulted to a balance of 75 units. Another receipt of inventory was gotten on 25thAugust of 50 units out of which 25 units were picked from here when the fourth issuance was made. So, after the last issuance, we had a balance of 150 units in total (made up of 50 units of 1st August batch, 75 units of 16thAugust inventory batch and 25 units of 25thAugust batch).

Note that the superscripts (i.e., *, ** ,1* and 2*) used below will guide you on which inventory batch each issuance was picked from. This inventory analysis is a computational proof of monetary value of closing inventory as at 30th/08/2021.