Merrick Differential Piece-Rate System: Definition; Formula; Examples; Advantages And Disadvantages

1.1 Definition:

Merrick Differential Piece-Rate System is methodology where by the employer pays the inefficient employee a minimum amount of income wage even if he or she accomplishes production of the expected output past the set or predetermined period.

Merrick Differential Piece-Rate System is Taylor’s differential piece-rate system modification which was developed by Merrick to solve the harsh and discriminative Taylor’s method of rewarding of employees.

1.2 Formula for Merrick Differential Piece-Rate System

So, how is the total wage income under Merrick Differential Piece-Rate System computed?

The progressive method uses a structure as follows;

Straight price up to X% of the standard output which is already pre-determined.

Between X% up to (X+Y) %, be paid above the normal production.

Any production >(X+Y) %, pay is above the rest previously mentioned.

In this scenario, three piece-rates are used to distinguish between the beginners, the average workers, and the superior workers, against two piece-rates in Taylor’s system.

In conclusion, this improved Tylor’s payment scheme will for instance pay the straight price rate up to let say 75% of the standard output, 15 % above the normal rate for producing between 75% – 100% and 25% above the normal rate for producing more than 100% of the pre-determined performance in terms of total output.

EXAMPLE ONE

Standard Output (i.e., children Toys) = 1,000 units

Piece-rate = $10

Terms and condition of Merrick Differential Piece-Rate System

If Production level is less than

85% of the standard output- pre-determined wage rate per children Toy is $0.10

If Production is between

85% and less than 100% of the standard output- wage rate per children Toy is $0.10 plus 10% of the $0.10 (i.e., normal pay).

Production

Above 100% of the standard output- wage rate per children Toy is $0.10 plus 20% of the $0.10 (i.e., normal pay).

Scenario (1): Output = 800 children Toys

Efficiency = 800/1,000 x 100 = 80%

Since the efficiency is less than 85%, the worker is paid only the basic rate, i.e., $0.10. therefore, the total wage income in this scenario will be;

Thus, income will be 800*$0.10)

=$80

NB: You can see that in this method, there is no punitive element for the employer did not lower the wage rate or rather has just used the already pre-determined one.

Scenario (2): Output= 900 children Toys

Efficiency = 900/1,000 x 100 = 90%

As the efficiency is more than 85% but less than 100 percent, employee to receive 10% above the normal rate. Thus,

Wage income = 900*0.11

= $99.00 Note that: ($0.11= 0.1 + (10%*0.10))

Scenario (3): Output = 1,100 units

Efficiency = 1,100/1,000 x 100 = 110%

As the efficiency is 110%, 20% above the normal rate is paid to the worker. Thus,

Wage income = 1100*0.12

=$132 Note that: ($12= 0.1 + 20%*0.10).

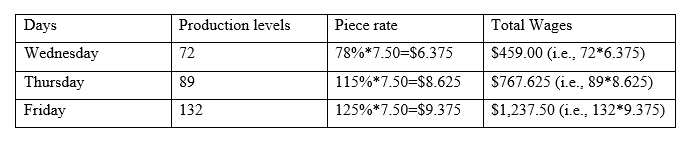

EXAMPLE TWO

Raphael works with Molasses metal fabricators and the terms of payment and output are as outlined below

|

Output % Standard

|

Payment

|

|

Up to 78%

|

Ordinary piece rate 100 units per day @$7.50

|

|

78% to 100%

|

115% of ordinary piece rate

|

|

Above 100%

|

125% of Ordinary Piece Rate

|

The management’s expected output per day to be 4 windows which is equivalent to100% level of output. Anything more than this per day is highly paid and equally anything less than this is lowly paid.

The production history of Raphael for the last THREE days was as follows

Production schedule for 3 days

Advantages of using Merrick Differential Piece-Rate System to Compute Labor Cost

- Merrick Differential Piece-Rate System promotes both efficient and inefficient workers for their performance.

- This approach eliminates the discriminative viewpoint commonly practiced in many organizations.

- Merrick Differential Piece-Rate System promotes a direct incentive to work for all employees which increase output in the long-run.

- The method treats all the employees equally and as a result, overall output increases even if it is in different proportions.

- Merrick Differential Piece-Rate System enhances or makes it easier to compute Cost per unit.

- Merrick Differential Piece-Rate System is not worker discriminative at the work place. So, it is a tool for employee motivation to all.

Disadvantages of using Merrick Differential Piece-Rate System to compute Labor Cost

-

Merrick Differential Piece-Rate System encourage employees to be lazy.

-

Merrick Differential Piece-Rate System demoralizes the more active employees.