Accounts Receivable

Definition-1 Accounts Receivable is the amount of cash not yet received from trade debtors for goods sold to them on credit by the business in question. Accounts receivable arise as a result of the business aiming to increasing its market share. Sometimes the instrument use is referred to trade debtors. Accounts receivables is classified as current asset in the balance sheet.

Or

Definition-2 Accounts receivable (AR) is the balance of money due to a firm for goods or services delivered or used but not yet paid for by customers. AR is any amount of money owed by customers for purchases made on credit. Accounts Receivable together with other financial instruments is used by lenders to assess the level of liquidity of a business

Or

Definition-3 Accounts Receivable is any cash or non-cash resource(s) your clienteles owe you for products (ie goods or services) they procured from the business in question. The amount owing from the customer is usually collected within a short duration such as weekly, fortnight or no monthly basis.

Accounting treatment of accounts receivable

Accounts Receivable is a current asset and it arises when the business in question sells goods or services on credit.

Example

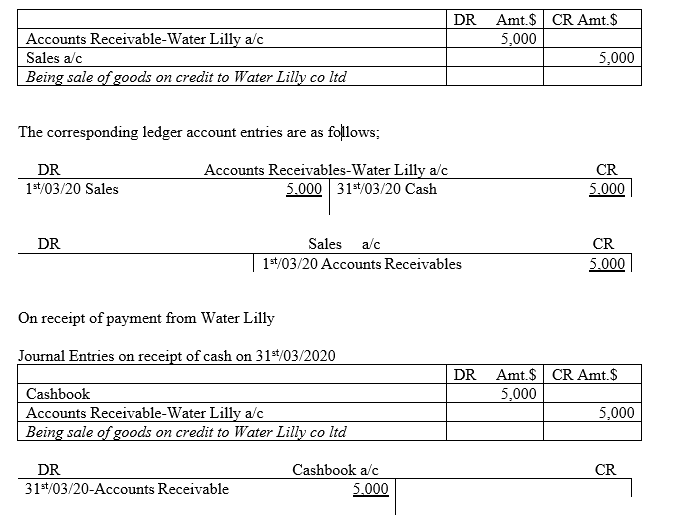

1st/03/2020 Water Tight co ltd sold goods worth $5,000 to Water Lilly co ltd on credit. The terms of payment was a one-month grace period. Water Lilly co ltd, the trade debtor (representing Accounts Receivable) did pay the amount due on 31st/03/2020 by cash.

Required

Show both the journal and ledger account entries as per the above transactions

Solution

On selling the goods on credit

Journal Entries on sell by credit

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.

About the Author - Dr Geoffrey Mbuva(PhD-Finance) is a lecturer of Finance and Accountancy at Kenyatta University, Kenya. He is an enthusiast of teaching and making accounting & research tutorials for his readers.