Rowan System: Definition; Characteristic; Formula; Example; Advantages And Disadvantages

1.1 Definition:

Rowan System is a plan for rewarding employees where by the method advocates that an employee be paid according to the time rate set if he or she takes more than the set period to finish the task. But a bonus is tied on one’s salary if the same task is accomplished within a shorter time than stipulated.

1.2 Characteristics of Rowan System or Plan

- Proportionality in rewarding of the employees

Rowan System advocates for computing the bonus as a proportion of the wages of time taken. In other words, bonus payment is based on that proportion of the time wages which the time saved bears to the standard time.

- Employees are guaranteed some income

There is a fixed day-wage for actual time taken on the basis of time rate that the employer promises the workers. This promotes the job security of the worker.

- Standardization of working time

The employer always sets a time benchmark as a standard timeframe for guiding on the thresholds within which a bonus is termed as valid.

- Bonus is characterized by a 50% of the time saved by a particular employee.

If a worker takes less than standard time, he is paid a bonus equal to 50%. This implies that the hard-working employee goes home with the normal salary plus a bonus.

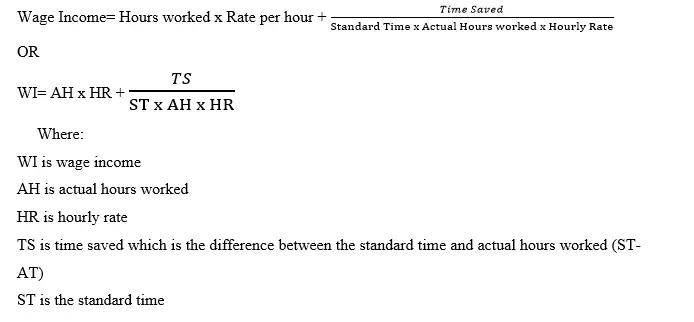

1.3 Formula for Rowan System or Plan or Method

So, how is the total wage income under Rowan System computed?

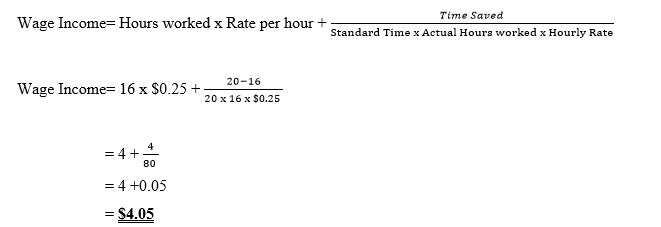

EXAMPLE

Bosco worked for 16 hours to complete a task assigned to him. The standard time set was 20 hours and with an hourly rate of $0.25 per hour. Using ROWAN PLAN, determine the total wages paid to Bosco.

Solution

1.3.1 Advantages of using Rowan System to Compute Labor Cost

1.Promotion of employee job security

The minimum hourly rate given by the employer makes the workers settle down and avoid running away from the company to look for greener pastures.

2.Output quality promotion

By giving such an attractive bonus, the employees in return do quality work or service provision to the organization. Hence increasing profitability.

3.Reduction of both labor cost and fixed overhead cost per unit

The 50% bonus aspect reserved by the organization after paying the other 50% bonus has cost reduction implications to the organization.

4.The method is simple to comprehend

This approach is used to compute the reward and the normal wage is not a complex one. Therefore, it is appreciated by all the stakeholders who make use of it.

5, Not punitive to the employee

The employer spares the employee the pain of being paid less income due to low performance. This idea is welcomed by all the workers for it is human.

6, Increased productivity

The organization in the overall registers increased output from both the efficient and the inefficient employees for as the active ones are being highly rewarded, also, the less active ones are spared form any punitive action by the employer.

7, Time saving

This method of rewarding employees saves time for the organization and hence more other activities can be attended to within the same time line.

1.3.2 Disadvantages of using Rowan System to Compute Labor Cost

- It is not a popular method amongst the employees. So, it is not commonly adhered to by them. This is because it is complex.

- Rewarding of the employee efficiency is limited to some point. That is, the system fails to distinguish between a very efficient worker and a worker with a less than mean efficiency.

- Employees not happy when the employer retains some amount of cash for employees fail to get the full returns of their endeavors.