What is a sales day book?

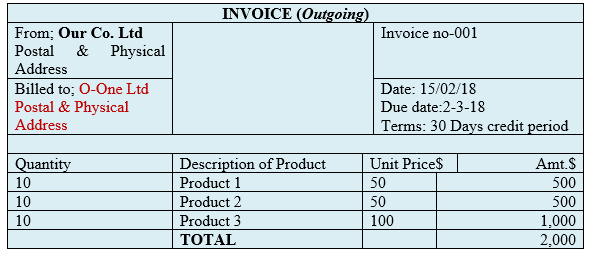

This is a book of original entry which is used to record information from the outgoing invoice(Stage three: Sale of Goods on Credit). It should be noted that this time round, Our Co. ltd is the seller of goods and is the one who prepares the outgoing invoice. Again, in level one of this tutorial series, we first considered sale of goods to only one buyer (sundry debtor-O ltd). In this case we further consider a case where by the seller has sold goods to several debtors. Ie In this case, we will assume that the goods were sold to different debtors (ie O limited is sundry debtors). That is, the transactions between Our Co. ltd and O ltd where made up of five debtors, namely; O-1, O-2, O-3, O-4 and O-5. Also the details of the goods sold to each creditor is shown in the respective source document. Hence Our Co. ltd prepares invoices (out coming) for each debtor. Therefore, the following is a demonstration of the link between the respective source document and the book of original entry that is used.

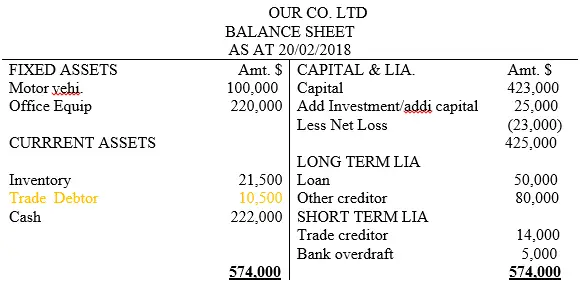

The learner is advised to re-visit the illustration three given in level one book and cross-examine the workings and the entries made in the respective ledger accounts so as to be conversant for the next illustration given in this section of level two tutorials is an expansion of the illustration three in level one. There we go now. The balance sheet and the specific debtor ledger account extract are as indicated whereby the trade debtor account of our concern is shaded using orange color.

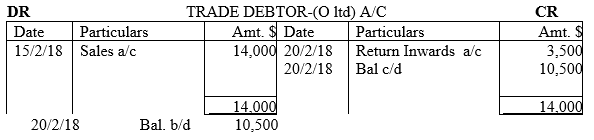

The trade debtor extract is as shown below;

NB:That the sales amount of $14,000 is the total amount of the goods that were sold by Our Co. ltd on 15/2/18 on credit to O ltd, although goods worth $3,500 were returned to the business on 20-02-2018. Let us now assume that the goods were not sold one debtor and that several buyers returned some of the goods to the seller (ie Our Co. ltd) as shown in illustration three

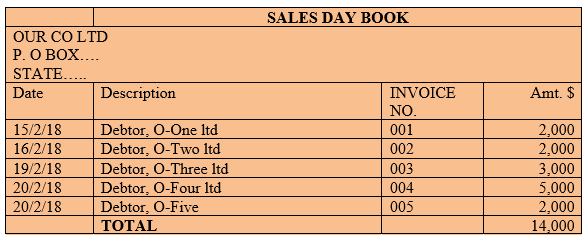

Sales day book example

Our Co. ltd sold goods on credit to FIVE different customers as follows;

15th/02/18 sold goods on credit to O-One limited for $2,000

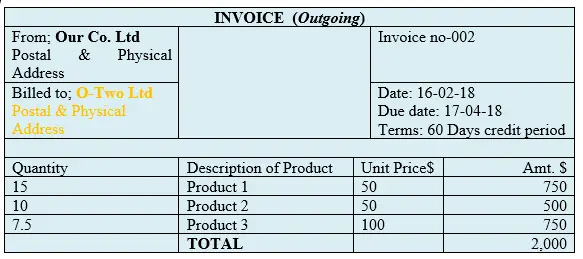

16th/02/18 sold goods on credit to O-Two limited for $2,000

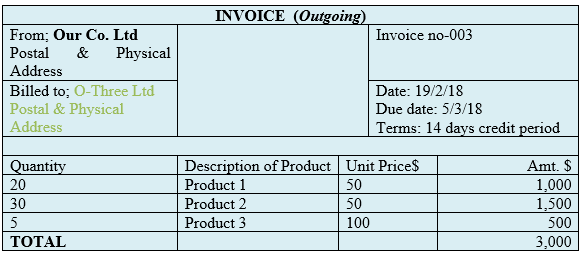

19th/02/18 sold goods on credit to O-Three limited for $3,000

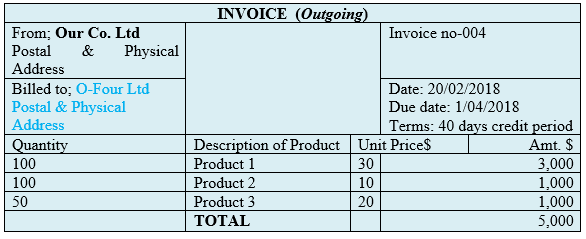

20th/02/18 sold goods on credit to O-Four limited for $5,000

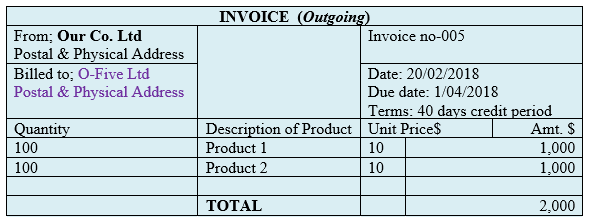

20th/02/18 sold goods on credit to O-Five limited for $ 2,000

NB: That Our Co. ltd (seller) will prepare and sent respective invoices (outgoing) to the five customers which will be of the SAME format. The learner need to remember that for the incoming invoice, the format were different even the serial numbers indicated in each document. Therefore, the corresponding invoices that will be sent by Our Co ltd to the five buyers will be as follows;

15th/02/18 sold goods on credit to O-One limited for $2,000

16th/02/18 sold goods on credit to O-Two limited for $2,000

19th/02/18 sold goods on credit to O-Three limited for $3,000

20th/02/18 sold goods on credit to O-Four limited for $5,000

20th/02/18 sold goods on credit to O-Five limited for $ 2,000

The corresponding book of original entry where the information in the various invoices are transferred to is the Sales Day Book or journal as shown below;